This article focuses on the accounting for defined benefit plans. It is a continuation of our earlier article on employee benefits. If you are first time on this topic or may have missed it, we suggest you to check out Accounting for Employee Benefits in our Accounting section.

In that article, we explained that there are four types of employee benefits. One of them is post-employment benefits. The accounting for post-employment benefits depends whether they are defined contribution plan or defined benefits plans. The accounting is straight-forward for defined contribution plan and we have explained the accounting requirements in detail in that article.

For this round, we going to provide you the key principles in accounting for defined benefit plans. Let’s now get into the details.

What is a defined benefit plan?

A defined benefit plan is an employee benefit plan where an entity’s obligation is to provide the agreed benefits to employees. Employees can either be the current or previous employees. Because of such an obligation, the entity is exposed to actuarial risk and investment risk. This means, an entity’s obligation may increase if actuarial or investment experience are worse than expected.

In providing defined benefit plan to employees, an entity may also subscribe to multi-employer plans. A multi-employer plan is the plan that:

- Firstly, pool the assets contributed by various entities that are not under common control.

- Secondly, use those assets to provide benefits to employees of more than one entity. For this, the contribution and benefits level are determined without regard to the identity of the entity that employs the employees.

For multi-employer plan, IAS 19 requires an entity to account for its proportionate share of the defined benefit obligation, plan assets and costs associated with the plan in the same way as for any other defined benefit plan. However, it is also possible for an entity not to have sufficient information to use defined benefit accounting for a multi-employer defined benefit plan. For instance, an entity has a restricted or limited access to the necessary information about the plan. In such a situation, an entity accounts for the plan as if it were a defined contribution plan.

The steps in accounting for defined benefit plans

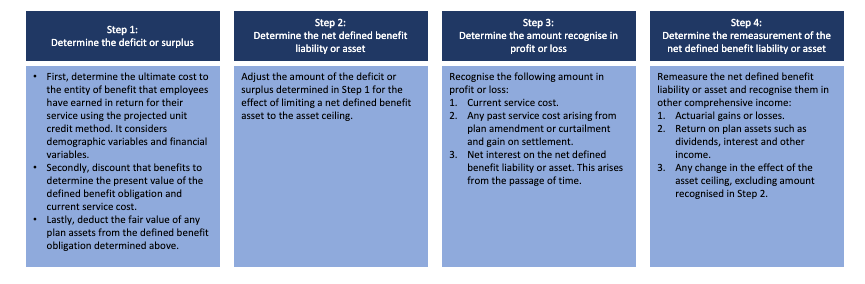

We have explained briefly in the earlier article that there are four steps to account for defined benefit plans. They are as follows:

- Firstly, an entity determines the deficit or surplus.

- Secondly, an entity determines the amount of net defined benefit liability or asset.

- Thirdly, an entity determines the amount to be recognised in profit or loss.

- Lastly, an entity determines the remeasurements of the net defined benefit liability or asset.

Let’s see each of the step in detail.

Step 1: Determine the deficit or surplus

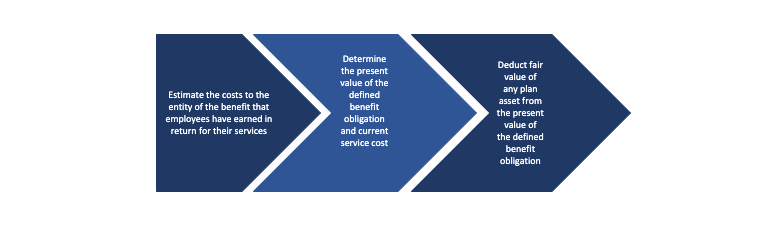

As a general understanding, deficit or surplus is the present value of defined benefit obligation less the fair value of plan assets. There are three critical processes to determine the deficit or surplus as follows:

Estimate the ultimate costs to the entity

First of all, entities need to make a reliable estimate of the ultimate cost of the benefits that employees have earned in return for their services. The estimate includes services provided in the current and prior periods. For this, entities use an actuarial technique, the projected unit credit method to estimate. Using the actuarial technique, entities are required the use various actuarial assumptions relating to demographic variables (such as employee turnover and mortality) as well as financial variables (such as discount rates, future salary increases and medical costs). These assumptions affect the cost of the benefit obligation.

IAS 19 provides specific guidance on the following actuarial assumptions:

A) Mortality

In determining the mortality assumption, entities refer to its best estimate of the mortality of plan members both during and after employment.

B) Discount rate

IAS 19 requires entities to determine the rate by reference to market yields at the end of the reporting period on high quality corporate bonds. For currency with no deep market in such high quality corporate bonds, entities use the market yield on government bond denominated in that currency instead. In practice, the real problem arises when there may be no bond with a sufficiently long maturity to match the estimated maturity of all the benefits payments. For this, IAS 19 allows an extrapolation of current market rates along the yield curve.

C) Salaries, benefits and medical costs

IAS 19 requires the assumptions used to measure defined benefit obligations to reflect:

- The benefits set out in the terms of the plan, including resulting from any constructive obligation that goes beyond terms of the plan, at the end of the reporting period.

- Estimated future salary increases that affect benefits payable (if any).

- The effect of any limit on the employer’s share of the cost of the future benefits.

- Contribution from employees or third parties that reduce the ultimate cost to the entity.

- Estimated future changes in the level of any state benefits that affect the benefit payable under the defined benefit plan.

Present value of defined benefit obligation and current service cost

The second step then is for entities to discount that benefit in order to determine the present value of the defined benefit obligation and the current service cost. Importantly, entities need to discount the whole of the post-employment benefit obligation even if entities expect to settle part of the obligation before 12 months after the reporting period. Entities use the same discount rate as explain in the actuarial assumptions.

Deduct fair value from the present value of the defined benefit obligation

Finally, entities deduct the fair value of any plan asset from the present value of the defined benefit obligation. Plan assets comprise assets held by a long-term employee benefit fund as well as qualifying insurance policies. Plan assets exclude unpaid contributions due from the reporting entity to the fund. Entities also reduces any liabilities of the fund that do not relate to employee benefits from the plan assets. Entities measure the fair value in accordance with IFRS 13 Fair Value Measurement.

In certain defined benefit plan, entities may also entitle for reimbursements. When entities are virtually certain that another party will reimburse some or all of the expenditure required to settle a defined benefit obligation, entities recognise their right to reimbursement as a separate asset. Entities measure this asset at fair value.

Step 2: Determine the amount of net defined benefit liability or asset

In the next step, entities need to determine the amount of the net defined benefit liability or asset. This amount is recognised in the statement of financial position. A net defined benefit liability or asset is the amount of the deficit or surplus determined in Step 1, adjusted for any effect of limiting a net defined benefit asset to the asset ceiling.

What is asset ceiling? Asset ceiling is the present value of any economic benefits available in the form of refunds from the plan or reduction in future contributions to the plan. Entities apply the same discount rate determined for actuarial assumption to derive to the present value of the asset ceiling.

Step 3: Determine the amount to be recognised in profit or loss

This step determines what goes to or recognise in profit or loss. Entities recognise the following in profit or loss:

- First, the current service cost.

- Secondly, any past service cost and gain or loss on settlement.

- Lastly, net interest on the net defined benefit liability or asset.

Let’s understand them.

The current service cost

First, the current service cost. This cost is the increase in the present value of the defined benefit obligation in the current period. Entities measure such cost using actuarial assumptions determined at the start of the annual reporting period unless entities remeasure the net defined benefit liability or asset.

The projected unit method used as the actuarial technique, requires entities to attribute benefits to the current period (for current service cost) and the current and prior periods (for defined benefit obligation). Entities attributes benefits to periods in which the obligation to provide post-employment benefits arises.

Entities attribute benefits based on the plan’s benefit formula. However, if an employee’s service in later years lead to a materially higher level of benefit that in earlier years, an entity attributes benefit on a straight-line basis from:

- The date when the service first leads to benefits under the plan until

- The date when further service lead to no material amount of further benefits under the plan.

Past service cost and gain or loss on settlement

The second item recognised in profit or loss is past service cost and gain or loss on settlement. In determining these, entities remeasure the net defined benefit liability or asset using the current fair value of plan asset and current actuarial assumptions. It includes using current market interest rates and current market prices reflecting the benefits offered under the plan and the plan assets before and after plan amendment, curtailment or settlement.

Past service cost

Past service cost is the change in the present value of the defined benefit obligation for employee service in prior periods. This change is due to a plan amendment or a curtailment. Plan amendment is the introduction, withdrawal of or changes to a defined benefit plan. On the other hand, curtailment is a significant reduction by the entity in the number of employees covered by a plan.

Entities recognise past service cost at the earlier of the following dates:

- When the plan amendment or curtailment occurs

- The recognition of related restructuring costs or termination benefits.

Gains or losses on settlement

Gains or losses on settlement is recognised when the settlement took place. Entities compute the amount as the difference between the present value of the defined benefit obligation being settled and the settlement price.

Net interest on the net defined benefit liability or asset

Lastly, entities also recognise net interest on the net defined benefit liability or asset. This is the changes due to passage of time.

Step 4: Determine the re-measurements of the net defined benefit liability or asset

This is the last step to account for define benefit plan. In this last step, IAS 19 requires entities to re-measure the net defined benefit liability or asset. The effect arising from re-measurement is recognised in other comprehensive income. Three items arise from the re-measurement:

- First, actuarial gains and losses.

- Second, return on plan assets.

- Third, any change in the effect of the asset ceiling.

Actuarial gains and losses are changes from increases or decreases in the present value of the defined benefit obligation due to changes in actuarial assumptions and experience adjustments. It does not include changes due to the introduction, amendment, curtailment or settlement of the defined benefit plan as explained in Step 3 above.

The return on plan assets are interest, dividends and other income derived from the plan assets, together with the realised and unrealised gains or losses on the plan assets. The amount is after deducting any costs of managing the plan assets and any tax payable on the plan itself. Other administrative costs are not deducted from the return on plan assets.

Summary

The above sums up the key principle in the accounting for defined benefit plans. The principles above may be overwhelming and because of that we have prepared for you the summary of steps and consideration for defined benefit plan below.

We will continue to bring you summary of key principles in our upcoming articles. Meantime, enjoy other articles in the Financial Accounting Section.