In this article, we bring to you the comparison of the accounting treatment for employee benefits in MPSAS 25, MFRS 119 and Section 28 of MPERS. What is employee benefit? Employee benefits are all forms of consideration given by an entity in exchange for service rendered by employees.

We have previously discussed the accounting for employee benefits under IAS 19. If you wish to refresh your understanding or first time on employee benefits topic, head out to Accounting for Employee Benefits. Take note that MFRS 119 is word-for-word IAS 19 following MFRS framework convergence with the International Financial Reporting Standards (“IFRS”).

For this article, we only discuss the significant differences noted in MPSAS 25 as compared to MFRS 119 and Section 28. This article will not discuss on how to determine which financial reporting framework an entity should use. If you have a question on this, head out to Financial Reporting Frameworks in Malaysia to read more. This comparison analysis is helpful for entities that are converting or thinking to convert from MPERS/MFRS framework to MPSAS.

Let’s now go into the details.

The scope of employee benefits

MPSAS 25, MFRS 119 and Section 28 state that there are four types of employee benefits as follows:

- Short-term employee benefits.

- Post-employment benefits.

- Other long-term employee benefits.

- Termination benefits.

There are no other significant differences in relation to the scope of employee benefits between the three standards.

Comparison of the accounting for employee benefits

Let’s now understand the comparison of the accounting for employee benefits under the three standards.

Comparison of short-term employee benefits

Under MPSAS 25 and Section 28, entities consider employee benefits as short-term if they are due to be settled within 12 months after the end of the period. Although MFRS 119 uses the term “before 12 months after the end of the annual reporting period”, we do not expect this to lead to any significant differences.

All three standards require entities to recognise their short-term employee benefits at an undiscounted amount that entities are expected to pay in exchange for the employees’ services. For this, entities to:

- recognise a liability after deducting any paid amount.

- recognise as an expense unless another standard requires or permits its capitalisation in the cost of an asset.

It is also worth noting that there are no significant differences in the accounting for both compensated or paid absences as well as profit sharing and bonus plans. In general, entities account for these benefits as summarised in the table below:

| Benefits | Accounting treatment |

|---|---|

| Non-accumulating compensated or paid absences | Entities recognise the cost when the absences occur. |

| Accumulating compensated or paid absences | Entities recognise the expected cost when the employees render service that increases their entitlement to future compensated or paid absences. Entities measure such cost as the additional amount that the entities expect to pay as a result of the unused entitlement that has accumulated at the end of the reporting date. |

| Profit-sharing and bonus plans | Entities recognise these benefits when and only when: – The entities have present legal or constructive obligations to make such payments as a result of past events; and – A reliable estimate of the obligation can be made. |

All three standards also do not provide any specific disclosures for short-term employee benefits.

Comparison of post-employment benefits

Let’s now move on to the comparison of the second type of employee benefits, the post-employment benefits.

The three standards require entities to account for post-employee benefits based on the economic substance of the plan. For this, post-employment benefits are classified either as defined contribution plans or defined benefit plans.

Under the defined contribution plans, entities’ obligations are limited to the amount that they agree to contribute to the funds. In contrast, under the defined benefit plan, entities’ obligations are subjected to actuarial risk and investment risk. This difference results in different accounting treatment to reflect the cost of post-employment benefits as discussed below.

MPSAS 25 also discusses on other schemes of post-employment benefits as follows:

- Multi-employer plans – an entity accounts for it based on its assessment whether it is a defined contribution plan or defined benefit plan.

- State plans – an entity accounts for it the same way as the multi-employer plan.

- Composite social security programs – an entity accounts for it the same way as the multi-employer plan.

- Insured benefits – an entity accounts for it as a defined contribution plan unless it has a legal or constructive obligation to pay employee directly when it is due or to pay further amount beyond amount contributed.

MFRS 119 and Section 28 also have the same accounting requirements as above, except that they do not have the composite social security program requirements.

Defined contribution plans

The accounting for defined contribution plan is straightforward because of the limit on entities’ obligations. Entities’ obligations are limited to the amounts contributed or to be contributed for the period. Accordingly, there is actuarial assumptions to measure the obligation or the expense. Besides, entities also measure the cost at an undiscounted amount.

All three standards require entities to recognise and measure contribution payable as a liability and an expense in exchange for the service they received during the period.

Defined benefit plans

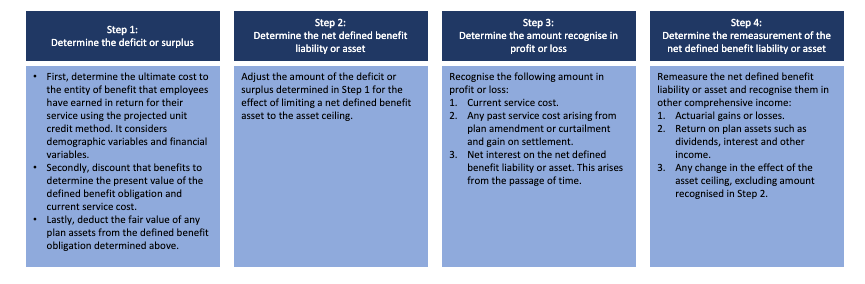

The accounting for a defined benefit plan is complex as it involves an actuarial method. We have explained in great length the accounting for defined benefit plan under IAS 19 in Accounting for Defined Benefit Plan. As the accounting requirement is complex, we suggest you have a read on that article first before you continue with the comparison between the three standards.

As a recap, MFRS 119 requires an entity to account for a defined benefit plan as follows:

MPSAS 25 however, requires an entity to consider the following in determining the defined benefit liability:

- Any actuarial gains (less actuarial losses) not recognised; and

- Minus any past service cost not yet recognised

Actuarial gains or losses

MFRS 119 and Section 28 do not allow for accumulation of actuarial gains or losses in the liability or asset. MFRS 119 requires the actuarial gains or losses to be recognised in other comprehensive income. Section 28 on the other hand, allows as an accounting policy choice, for entities to recognise the actuarial gain or loss in profit or loss or other comprehensive income.

To clarify, MPSAS 25 requires an entity to recognise a portion of its actuarial gains or losses as revenue or expense in surplus or deficit, if the net cumulative unrecognised actuarial gains and losses at the end of the previous reporting period exceeded the greater of:

- 10% of the present value of the defined benefit obligation at that date; and

- 10% of the fair value of any plan assets at that date.

Alternatively, an entity also has the option in MPSAS 25 to recognise the amount determined above directly in net asset/equity.

Past service cost

MPSAS 25 requires an entity to recognise past service cost on straight-line basis over the average period until the benefits become vested. Unlike MPSAS 25, entities expense of past service cost under MFRS 119 and Section 28. Also note that under MPSAS 25, past service cost does not include the effect from a curtailment. Whereas in MFRS 119, the effect from a curtailment is part of past service cost.

Other differences for defined benefit plans

MPSAS 25 also does not provide an explicit requirement for entities to consider mortality as one of the actuarial assumptions. The mortality assumption is, however, explicitly included in MFRS 119 and Section 28. In addition, MPSAS 25 does not explicitly require entities to use discount rates by reference to market yields on high-quality corporate bonds. Instead, MPSAS 25 only requires the discount rate to reflect the time value of money.

Comparison of other long-term employee benefits

MPSAS 25 requires entities to recognise as a liability the net total of the following amounts:

- The present value of the defined benefit obligation at the reporting date

- Minus the fair value of plan assets.

Entities using MFRS 119 or Section 28 also generally apply the same principles on this aspect.

For other long-term employee benefits, MPSAS 25 requires entities to recognise the net total of the following amount as an expense (unless another standard allows or permits its capitalisation):

- Current service costs

- Interest cost

- The expected return of any plan assets and on any reimbursement right recognised as an asset

- Actuarial gains and losses

- Past service cost

- The effect of any curtailments or settlements.

Generally, similar requirements are also applicable for MFRS 119 and Section 28.

Termination benefits

MPSAS 25 and Section 28 require an entity to recognise termination benefits as a liability and an expense only when entities are demonstrably committed to either:

- Terminate the employment before the normal retirement date, or

- Provide termination benefits as a result of an offer made to encourage voluntary redundancy.

Both standards explained that an entity is demonstrably committed only when the entity has a detailed formal plan for the termination as well as is without a realistic possibility of withdrawal.

MFRS 119 on the other hand, requires an entity to recognise a liability and an expense at the earlier of:

- The date when the entities can no longer withdraw the offer of those benefits; or

- When the entities recognise costs for a restructuring that is within the scope of MFRS 137 Provisions, Contingent Liabilities and Contingent Assets and involve the payment for termination benefits.

Entities can no longer withdraw the offer either when the employee accepts the offer or when a restriction on the entities’ ability to withdraw take effect (whichever the earlier).

As such, entities recognise termination benefits in MPSAS 25 and Section 28 based on management’s action – that the management is demonstrably committed. While in MFRS 119, the recognition is when an entity is unable to withdraw the offer of termination. Accordingly, it is possible to result in a timing difference in recognising the termination benefits.

Measurement of termination benefits

About the measurement, MPSAS 25 and Section 28 requires entities to measure termination benefits at the best estimate of the expenditure would be required to settle the obligation at the reporting date. In addition, for the offer made to encourage voluntary redundancy, entities measure the termination benefits based on the number of employees expected to accept the offer. Entities apply an appropriate discount rate when termination benefits are due more than 12 months after the end of the reporting period.

As for MFRS 119, the standard requires entities to measure the termination benefits based on the nature of employee benefits. This means entities apply the requirements for short-term benefits or other long-term benefits for termination benefits, depending on when entities expect to settle it. Nevertheless, we believe all three standards essentially require entities to apply the same measurement principle – i.e., to measure termination benefits based on the best estimate of the expenditure required to settle the obligation.

Conclusion

The above sums up the significant differences in the accounting for employee benefits under MPSAS 25, MFRS 119 and Section 28 of MPERS. The main accounting differences arise from the accounting for the defined benefit plan. The full MPSAS 25, MFRS 119 and Section 28 of MPERS are available on the respective issuing bodies website for your reference.

Note that at the international level, the revised IPSAS 39 Employee Benefits is very much aligned with the requirements in MFRS 119. Hence, the differences may no longer exist when Malaysia issues or adopts the revised standard.

We will continue to discuss other comparisons in our upcoming articles. Meanwhile, you can read other relevant articles in the Financial Accounting section.